tidymodels

Application Exercise

- Create a new project from this template in RStudio Pro:

- Load the packages and data by running the top chunk of R code

02:00

tidymodels

Linear Regression Model Specification (regression)

Computational engine: lm Validation set approach

A faster way!

- You can use

last_fit()and specify the split - This will automatically train the data on the

traindata from the split - Instead of specifying which metric to calculate (with

rmseas before) you can just usecollect_metrics()and it will automatically calculate the metrics on thetestdata from the split

A faster way!

set.seed(100)

Auto_split <- initial_split(Auto, prop = 0.5)

lm_fit <- last_fit(lm_spec,

mpg ~ horsepower,

split = Auto_split)

lm_fit |>

collect_metrics() # A tibble: 2 × 4

.metric .estimator .estimate .config

<chr> <chr> <dbl> <chr>

1 rmse standard 4.96 Preprocessor1_Model1

2 rsq standard 0.613 Preprocessor1_Model1What about cross validation?

What if we wanted to do some preprocessing

- For the shrinkage methods we discussed it was important to scale the variables

What does this mean?

What would happen if we scale before doing cross-validation? Will we get different answers?

What if we wanted to do some preprocessing

What if we wanted to do some preprocessing

recipe()!- Using the

recipe()function along withstep_*()functions, we can specify preprocessing steps and R will automagically apply them to each fold appropriately.

Where do we plug in this recipe?

- The

recipegets plugged into thefit_resamples()function

Auto_cv <- vfold_cv(Auto, v = 5)

rec <- recipe(mpg ~ horsepower, data = Auto) |>

step_scale(horsepower)

results <- fit_resamples(lm_spec,

preprocessor = rec,

resamples = Auto_cv)

results |>

collect_metrics()# A tibble: 2 × 6

.metric .estimator mean n std_err .config

<chr> <chr> <dbl> <int> <dbl> <chr>

1 rmse standard 4.91 5 0.233 Preprocessor1_Model1

2 rsq standard 0.615 5 0.0313 Preprocessor1_Model1What if we want to predict mpg with more variables

- Now we still want to add a step to scale predictors

- We could either write out all predictors individually to scale them

- OR we could use the

all_predictors()short hand.

Putting it together

rec <- recipe(mpg ~ horsepower + displacement + weight, data = Auto) |>

step_scale(all_predictors())

results <- fit_resamples(lm_spec,

preprocessor = rec,

resamples = Auto_cv)

results |>

collect_metrics()# A tibble: 2 × 6

.metric .estimator mean n std_err .config

<chr> <chr> <dbl> <int> <dbl> <chr>

1 rmse standard 4.24 5 0.206 Preprocessor1_Model1

2 rsq standard 0.711 5 0.0148 Preprocessor1_Model1 Application Exercise

- Examine the

Hittersdataset by running?Hittersin the Console - We want to predict a major league player’s

Salaryfrom all of the other 19 variables in this dataset. Create a visualization ofSalary. - Create a recipe to estimate this model.

- Add a preprocessing step to your recipe, scaling each of the predictors

06:00

What if we have categorical variables?

- We can turn the categorical variables into indicator (“dummy”) variables in the recipe

What if we have missing data?

- We can remove any rows with missing data

What if we have missing data?

Application Exercise

- Add a preprocessing step to your recipe to convert nominal variables into indicators

- Add a step to your recipe to remove missing values for the outcome

- Add a step to your recipe to impute missing values for the predictors using the average for the remaining values NOTE THIS IS NOT THE BEST WAY TO DO THIS WE WILL LEARN BETTER TECHNIQUES!

06:00

Ridge, Lasso, and Elastic net

When specifying your model, you can indicate whether you would like to use ridge, lasso, or elastic net. We can write a general equation to minimize:

\[RSS + \lambda\left((1-\alpha)\sum_{i=1}^p\beta_j^2+\alpha\sum_{i=1}^p|\beta_j|\right)\]

- First specify the engine. We’ll use

glmnet - The

linear_reg()function has two additional parameters,penaltyandmixture penaltyis \(\lambda\) from our equation.mixtureis a number between 0 and 1 representing \(\alpha\)

Ridge, Lasso, and Elastic net

\[RSS + \lambda\left((1-\alpha)\sum_{i=1}^p\beta_j^2+\alpha\sum_{i=1}^p|\beta_j|\right)\]

What would we set mixture to in order to perform Ridge regression?

Application Exercise

- Set a seed

set.seed(1) - Create a cross validation object for the

Hittersdataset - Using the recipe from the previous exercise, fit the model using Ridge regression with a penalty \(\lambda\) = 300

- What is the estimate of the test RMSE for this model?

06:00

Ridge, Lasso, and Elastic net

\[RSS + \lambda\left((1-\alpha)\sum_{i=1}^p\beta_j^2+\alpha\sum_{i=1}^p|\beta_j|\right)\]

Okay, but we wanted to look at 3 different models!

tune 🎶

- Notice the code above has

tune()for the the penalty and the mixture. Those are the things we want to vary!

tune 🎶

- Now we need to create a grid of potential penalties ( \(\lambda\) ) and mixtures ( \(\alpha\) ) that we want to test

- Instead of

fit_resamples()we are going to usetune_grid()

tune 🎶

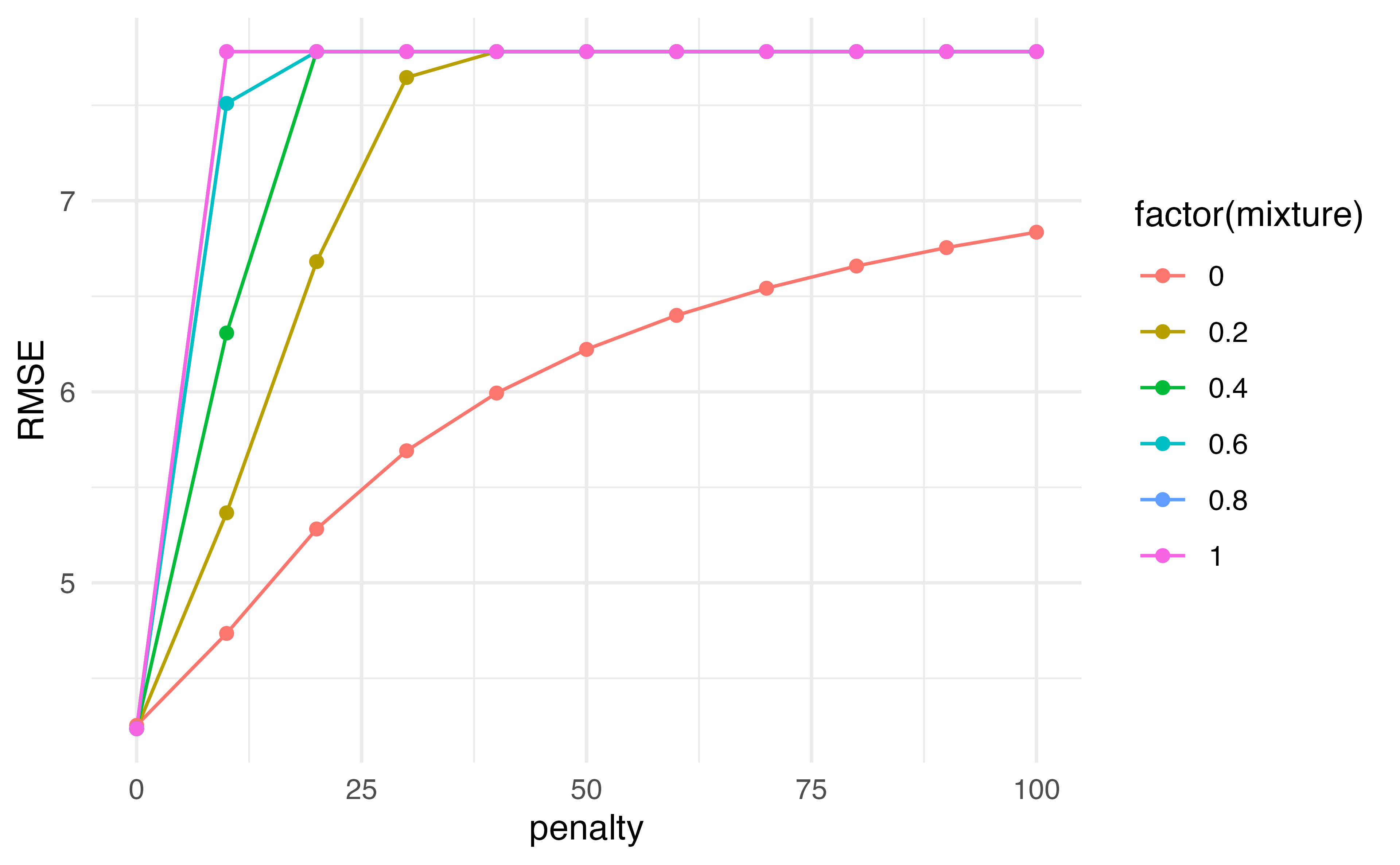

# A tibble: 132 × 8

penalty mixture .metric .estimator mean n std_err .config

<dbl> <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

1 0 0 rmse standard 4.25 5 0.217 Preprocessor1_Model01

2 0 0 rsq standard 0.710 5 0.0171 Preprocessor1_Model01

3 10 0 rmse standard 4.74 5 0.246 Preprocessor1_Model02

4 10 0 rsq standard 0.706 5 0.0193 Preprocessor1_Model02

5 20 0 rmse standard 5.28 5 0.255 Preprocessor1_Model03

6 20 0 rsq standard 0.705 5 0.0194 Preprocessor1_Model03

7 30 0 rmse standard 5.69 5 0.258 Preprocessor1_Model04

8 30 0 rsq standard 0.705 5 0.0195 Preprocessor1_Model04

9 40 0 rmse standard 5.99 5 0.260 Preprocessor1_Model05

10 40 0 rsq standard 0.705 5 0.0195 Preprocessor1_Model05

# … with 122 more rowsSubset results

# A tibble: 66 × 8

penalty mixture .metric .estimator mean n std_err .config

<dbl> <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

1 0 0.6 rmse standard 4.24 5 0.207 Preprocessor1_Model34

2 0 0.4 rmse standard 4.24 5 0.207 Preprocessor1_Model23

3 0 1 rmse standard 4.24 5 0.207 Preprocessor1_Model56

4 0 0.8 rmse standard 4.24 5 0.207 Preprocessor1_Model45

5 0 0.2 rmse standard 4.24 5 0.207 Preprocessor1_Model12

6 0 0 rmse standard 4.25 5 0.217 Preprocessor1_Model01

7 10 0 rmse standard 4.74 5 0.246 Preprocessor1_Model02

8 20 0 rmse standard 5.28 5 0.255 Preprocessor1_Model03

9 10 0.2 rmse standard 5.37 5 0.258 Preprocessor1_Model13

10 30 0 rmse standard 5.69 5 0.258 Preprocessor1_Model04

# … with 56 more rows- Since this is a data frame, we can do things like filter and arrange!

Subset results

# A tibble: 66 × 8

penalty mixture .metric .estimator mean n std_err .config

<dbl> <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

1 0 0.6 rmse standard 4.24 5 0.207 Preprocessor1_Model34

2 0 0.4 rmse standard 4.24 5 0.207 Preprocessor1_Model23

3 0 1 rmse standard 4.24 5 0.207 Preprocessor1_Model56

4 0 0.8 rmse standard 4.24 5 0.207 Preprocessor1_Model45

5 0 0.2 rmse standard 4.24 5 0.207 Preprocessor1_Model12

6 0 0 rmse standard 4.25 5 0.217 Preprocessor1_Model01

7 10 0 rmse standard 4.74 5 0.246 Preprocessor1_Model02

8 20 0 rmse standard 5.28 5 0.255 Preprocessor1_Model03

9 10 0.2 rmse standard 5.37 5 0.258 Preprocessor1_Model13

10 30 0 rmse standard 5.69 5 0.258 Preprocessor1_Model04

# … with 56 more rowsWhich would you choose?

results |>

collect_metrics() |>

filter(.metric == "rmse") |>

ggplot(aes(penalty, mean, color = factor(mixture), group = factor(mixture))) +

geom_line() +

geom_point() +

labs(y = "RMSE")

Application Exercise

- Using the

Hitterscross validation object and recipe created in the previous exercise, usetune_gridto pick the optimal penalty and mixture values. - Update the code below to create a grid that includes penalties from 0 to 50 by 1 and mixtures from 0 to 1 by 0.5.

- Use this grid in the

tune_gridfunction. Then usecollect_metricsand filter to only include the RSME estimates. - Create a figure to examine the estimated test RMSE for the grid of penalty and mixture values – which should you choose?

08:00

Putting it all together

- Often we can use a combination of all of these tools together

- First split our data

- Do cross validation on just the training data to tune the parameters

- Use

last_fit()with the selected parameters, specifying the split data so that it is evaluated on the left out test sample

Putting it all together

auto_split <- initial_split(Auto, prop = 0.5)

auto_train <- training(auto_split)

auto_cv <- vfold_cv(auto_train, v = 5)

rec <- recipe(mpg ~ horsepower + displacement + weight, data = auto_train) |>

step_scale(all_predictors())

tuning <- tune_grid(penalty_spec,

rec,

grid = grid,

resamples = auto_cv)

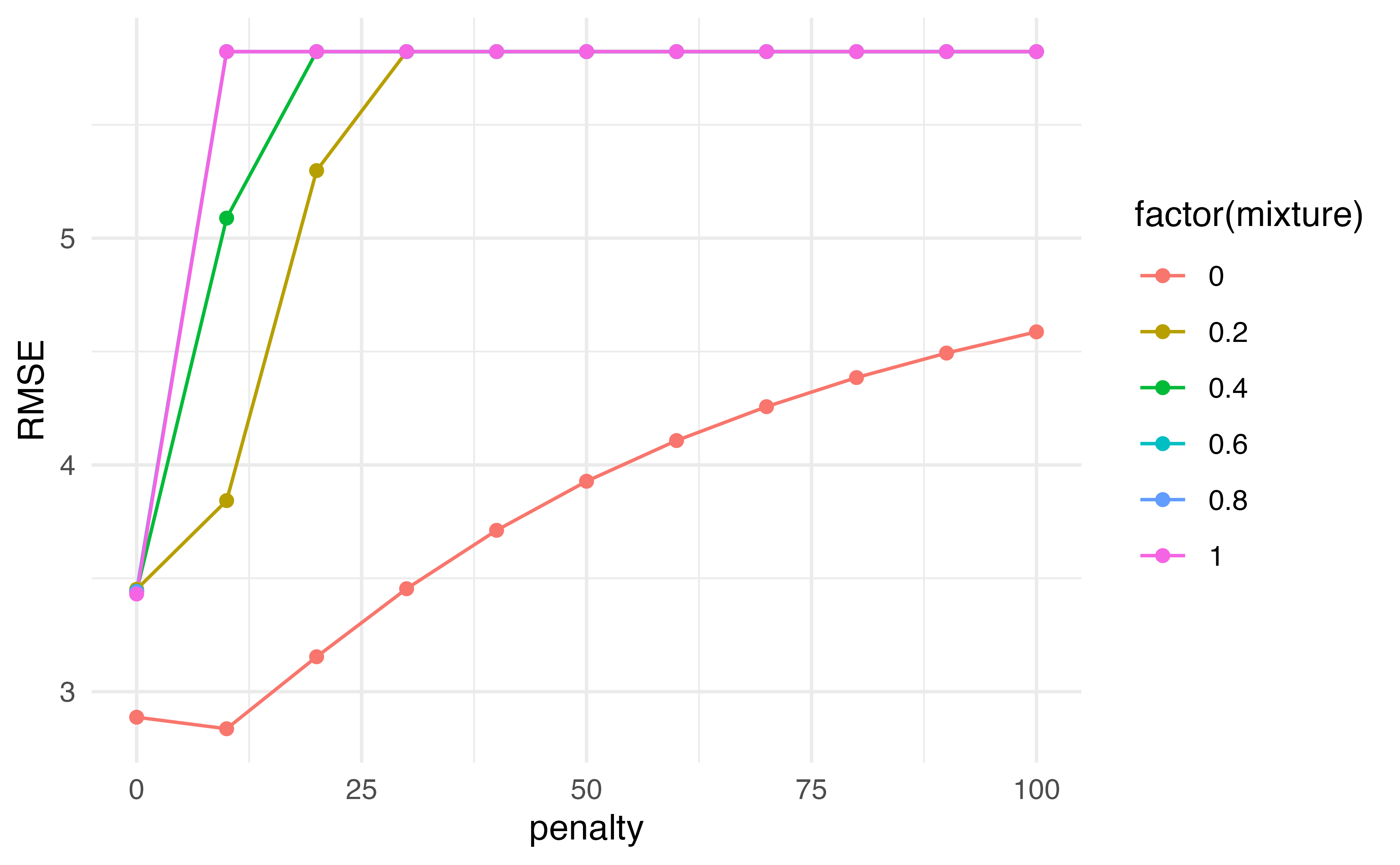

tuning |>

collect_metrics() |>

filter(.metric == "rmse") |>

arrange(mean)# A tibble: 66 × 8

penalty mixture .metric .estimator mean n std_err .config

<dbl> <dbl> <chr> <chr> <dbl> <int> <dbl> <chr>

1 0 1 rmse standard 4.52 5 0.105 Preprocessor1_Model56

2 0 0.6 rmse standard 4.52 5 0.105 Preprocessor1_Model34

3 0 0.8 rmse standard 4.52 5 0.106 Preprocessor1_Model45

4 0 0.2 rmse standard 4.53 5 0.104 Preprocessor1_Model12

5 0 0.4 rmse standard 4.53 5 0.104 Preprocessor1_Model23

6 0 0 rmse standard 4.54 5 0.132 Preprocessor1_Model01

7 10 0 rmse standard 5.01 5 0.232 Preprocessor1_Model02

8 20 0 rmse standard 5.54 5 0.266 Preprocessor1_Model03

9 10 0.2 rmse standard 5.63 5 0.271 Preprocessor1_Model13

10 30 0 rmse standard 5.94 5 0.280 Preprocessor1_Model04

# … with 56 more rowsPutting it all together

final_spec <- linear_reg(penalty = 0, mixture = 0) |>

set_engine("glmnet")

fit <- last_fit(final_spec,

rec,

split = auto_split)

fit |>

collect_metrics()# A tibble: 2 × 4

.metric .estimator .estimate .config

<chr> <chr> <dbl> <chr>

1 rmse standard 4.00 Preprocessor1_Model1

2 rsq standard 0.726 Preprocessor1_Model1Extracting coefficients

- We can use

workflow()to combine the recipe and the model specification to pass to afitobject.

Application Exercise

- Using the final model specification, extract the coefficients from the model by creating a

workflow - Filter out any coefficients exactly equal to 0

03:00

Dr. Lucy D’Agostino McGowan adapted from Alison Hill’s Introduction to ML with the Tidyverse